Father and Son Illustration

As your home grows in value and you amortize the amount of your mortgage, the equity grows in your home. If you were to reposition that equity by refinancing your home and investing the money, this can effectively become a vehicle to save money and accumulate assets. I will show you an example that is as simple as it is powerful. I have adapted it from the book, The New Rules of Money, by Ric Edelman.

Consider a father and a son. The father is stuck in the traditional way of thinking, the old way. He says:

“Pay off the mortgage as soon as possible!”

The son is more contemporary in his thinking. He believes in the new way. He says:

“Carry a big, long mortgage!”

Each of them earns $150,000 per year. They each have $100,000 in savings and both are buying a $500,000 home. The father gets a 15-year mortgage at an APR of 5.875%; the son gets a 30-year, interest-only loan at 6.375% APR. The father makes a big down payment of $100,000, while the son makes a small down payment of $25,000. This leaves the father with $0 to invest and the son with $75,000.

As a result, the father makes a monthly payment of $3,348, while the son makes a monthly payment of $2,523. Note that the son’s monthly payments are 100% tax-deductible, while the father’s are not, so the average monthly net after-tax cost for the father is $2,983, and the son’s is only $1,690. Big difference.

Each month, the father religiously sends in an extra $200 with his mortgage payment; the son puts his $200—plus the money he saves on his monthly mortgage payment, $1,293—into an investment that returns 6%. After 5 years, the son has accumulated $205,330 in his investment account while the father has accumulated only the equity in his home. In 13.75 years the father owns his home and due to the tax savings and investing in the same fund as his son, he now has an investment account worth $51,832. The son has made enough in his investment account that he can pay off his mortgage and still have $143,249 left over in his investment account.

So they both own their homes, but the son has a bigger investment asset.

In 30 years, the son has accumulated $1,951,434 in savings and investments, while the father has only $1,052,877—a difference of $898,557. The son is that much ahead.

What makes the difference?

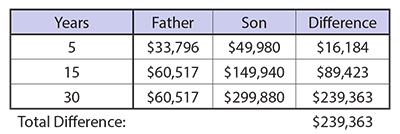

Behind the scenes, there is a significant tax advantage favoring the son, among other things. After 5 years, the son has received $49,955 in tax savings; the father, only $33,796. Here is the breakdown in tax savings:

Another benefit the son enjoys is this: He is better able to handle uncertainty.

Suppose, after five years, they both lose their jobs. The father has no savings to survive the crisis while the son has $205,330. The father can’t get a loan because he has no job; all that equity in his home does him no good. The son doesn’t need a loan. The father will be forced to sell his home or face foreclosure or a short sale because he cannot make his payments, while the son has no problem making his mortgage payments. The father is in panic mode; the son is not.